In his latest Quick Take, Ian Bremmer calls the United States under President Trump the dominant driver of global political risk, but argues that the world is increasingly pushing back.

In his latest Quick Take, Ian Bremmer argues that the war in Iran has exposed the limits of President Trump’s strategy of using maximum pressure to force adversaries into concessions.

The May jobs report showed 172,000 new positions added in the US, double what economists expected. So why do two-thirds of Americans say they're having a hard time finding a good job?

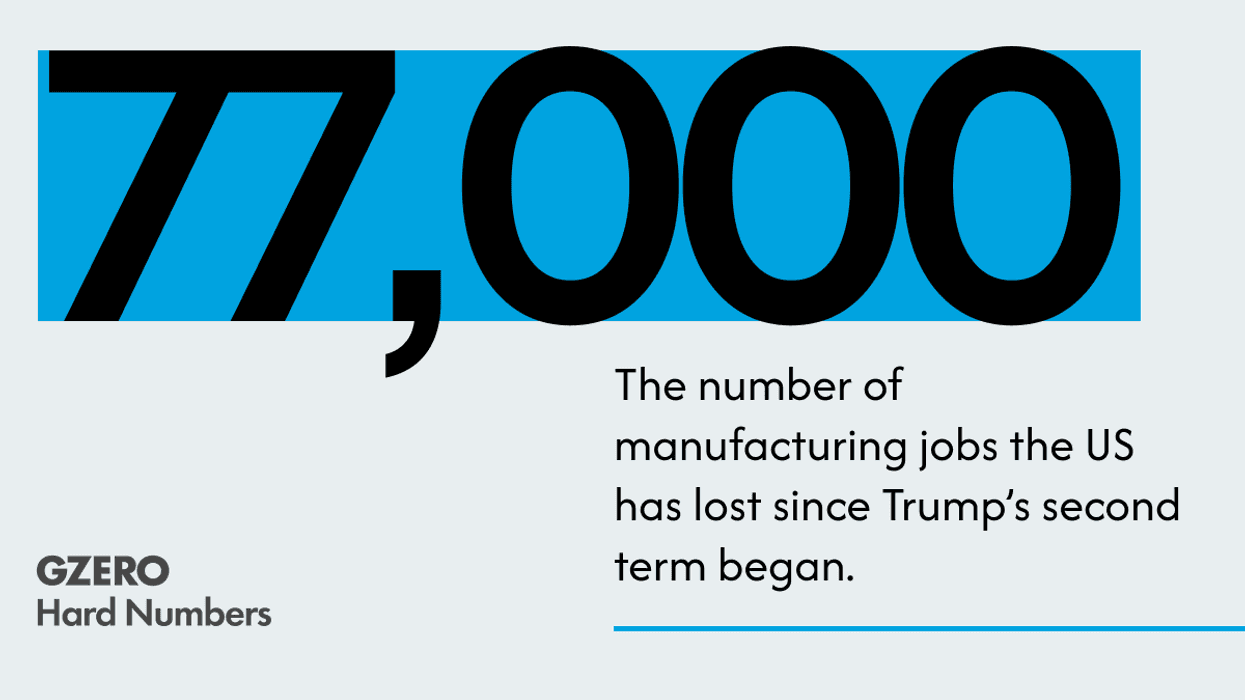

Investment in manufacturing construction has also fallen 16% during that period, despite public investment pledges of some $900 billion from companies.

In this episode of GZERO Europe, Carl Bildt examines how the war in Iran is driving up energy prices, fueling inflation, and raising stagflation fears across Europe.

Despite rising anti-globalization rhetoric in Washington, Americans continue to engage with the global economy according to Scott Lincicome and Paul Krugman.

The Supreme Court curbs Trump’s trade agenda, but the administration is undeterred. So, what's next? Ian Bremmer sits down with economists Scott Lincicome of the Cato Institute and Paul Krugman to examine the future of tariffs, and the politics shaping trade policy.